At some point in your career, you’ll likely find yourself considering a new opportunity and comparing job offers. It’s a big decision—and one we regularly help clients navigate, particularly those in their 30s, 40s, and 50s who are evaluating career changes alongside long-term financial goals.

The key question we often hear is: “Will this new role support or disrupt my financial plan?”

There are two primary ways to look at it:

Choose a job that aligns with your current goals.

Adjust your goals to reflect new priorities—for instance, trading higher college savings for more time with family.

Our role is to help you weigh these trade-offs with clarity and confidence.

To help organize your thinking, we’ve created a downloadable worksheet that outlines key factors to consider—both financial (salary, benefits, equity, etc.) and intangible (culture, flexibility, growth potential).

Here’s how to make the most of it:

Fill out what you know—any blanks may point to questions you’ll want to ask the employer.

Highlight what matters most—whether that’s compensation, purpose, or professional development.

Talk it through—with a partner, mentor, or financial advisor. A second perspective can provide valuable clarity.

Changing jobs is rarely a black-and-white decision. But documenting the trade-offs and staying focused on what truly matters can bring much-needed perspective.

At Commas, we help clients keep their financial goals front and center. If a new opportunity moves you closer to the life you envision then it may be the right next step. Looking for guidance as you compare job offers? Let’s talk about how we can help.

Commas is a wholly-owned subsidiary of Truepoint Inc., a fee-only Registered Investment Adviser (RIA). Registration as an adviser does not connote a specific level of skill or training nor an endorsement by the SEC. More detail, including forms ADV Part 2A and Form CRS filed with the SEC, can be found at www.usecommas.com. Neither the information, nor any opinion expressed, is to be construed as personalized investment, tax or legal advice. The accuracy and completeness of information presented from third-party sources cannot be guaranteed.

Subscribe to newsletter

Subscribe to receive the latest blog posts to your inbox.

When thinking about your financial priorities, retirement may not be top of mind–especially if you’re in your early or mid-career and focused on shorter term goals like buying a home, managing student debt, or saving for your kids’ education. While retirement may seem a long way off, your early career is actually the ideal time to start saving into a Roth IRA so you can take advantage of a lower tax bracket, a long investment horizon, and years of compound interest.

How It Works

A Roth IRA is an individual retirement account funded with after-tax income. Since the money has been taxed before contribution, you’ll never be taxed on those funds again and your investments will grow tax-free, and withdrawals in retirement are also tax-free.

Unlike workplace retirement plans like a 401(k), a Roth IRA is also owned personally, giving you greater flexibility when it comes to managing your account. This also means you have the ability to contribute the maximum into both your employer 401k and Roth IRA.

Key Benefits of a Roth IRA

Tax-Free Growth & Withdrawals: Contributions are made with after-tax dollars, so you won’t pay taxes on your investment gains or qualified withdrawals (and neither will your beneficiaries).

Penalty-Free Contribution Withdrawals: You can withdraw the amount you’ve contributed at any time without tax or penalties, but withdrawing earnings before retirement (or age 59.5) may have restrictions.

No Required Minimum Distributions (RMDs): Unlike traditional retirement accounts, you’re not required to withdraw funds at a certain age, allowing your savings to continue growing tax-free.

Roth IRA vs. Traditional IRA

Both Roth and traditional IRAs help you save for retirement, but they differ in tax treatment:

Traditional IRA: Contributions are tax-deductible now, but withdrawals in retirement are taxed as income.

Roth IRA: Contributions are taxed upfront, but withdrawals in retirement are tax-free.

Contribution & Withdrawal Rules

Income Limits: Contribution eligibility depends on income. In 2025, individuals earning under $150,000 or married couples earning under $236,000 can contribute up to $7,000 annually (or $8,000 if age 50+).

Withdrawal Rules: Contributions can be withdrawn anytime without penalty, but withdrawing earnings before age 59.5 may result in taxes or penalties unless certain conditions are met.

Backdoor Roth IRA:High earners above the income limits may still contribute through a strategy called a Backdoor Roth IRA.

Inherited Rules: Congress has passed a law requiring inherited Traditional and Roth IRAs be emptied in 10 years. When you pass down a Roth IRA, your heirs will be able to make tax-free withdrawals (instead of the taxed withdrawals they would be making from a Traditional IRA), saving them significant taxes—and effectively providing them a larger inheritance!

When to Start a Roth IRA

The best time to start is as soon as possible! As long as you have earned income, you can contribute to a Roth IRA now so you can reap the benefits later. Additionally, contributions for the previous year can be made until the tax filing deadline (April 15).

How to Open a Roth IRA in Four Steps

Choose a Provider: Select a trusted financial institution and review any fees.

Complete the Setup: Provide your Social Security number, banking details, and beneficiary information.

Select Investments: Align your portfolio with your risk tolerance and time horizon.

Set Up Contributions: Choose a lump sum or automatic monthly contributions.

Is a Roth IRA Right for You?

Want to build wealth long-term, but don’t have the spare time or mental resources to dedicate to investigating all of your options, building out a plan, and reorganizing your finances? We can help.

Commas is a wholly-owned subsidiary of Truepoint Inc., a fee-only Registered Investment Adviser (RIA). Registration as an adviser does not connote a specific level of skill or training nor an endorsement by the SEC. More detail, including forms ADV Part 2A and Form CRS filed with the SEC, can be found at www.usecommas.com. Neither the information, nor any opinion expressed, is to be construed as personalized investment, tax or legal advice. The accuracy and completeness of information presented from third-party sources cannot be guaranteed.

Subscribe to newsletter

Subscribe to receive the latest blog posts to your inbox.

One of the most compelling aspects of Google’s compensation packages is the awarding of Restricted Stock Units (RSUs)—or Google Stock Units (GSUs) as employees like to call them. This amazing benefit comes with unique financial planning opportunities, including an asymmetrical vesting schedule, new tax obligations, limited selling windows, and possible enrollment in the Employee Trading Plan (ETP). Here at Commas, we are here to help you understand and navigate your GSUs.

Understanding the GSU Basics

GSUs are a type of equity compensation that gives employees the promise of Alphabet shares (GOOG) at a future date. You can be awarded GSUs at key moments—for example, when you’re hired or with your annual salary increase. These GSUs vest over time, and once they vest, they are yours, like any other stock you purchase. When they are awarded to you, the company indicates what the GSUs are worth at that time, noting that the value may differ upon vesting. This makes them a variable addition to your compensation package, subject to stock volatility.

Historically, Google employees have received two kinds of shares: GOOGL (comes with voting rights, no longer distributed) or GOOG (no voting rights, still distributed). Employees’ vested shares are held in custody at Morgan Stanley. To view or sell your vested shares, sign into the Morgan Stanley portal.

Key RSU Terms

Here are the key terms to understand:

Grant Agreement: the document that outlines the conditions of your RSUs – number of shares granted, vesting period, etc.

Grant Date: the date Google awards RSUs to an employee

Vesting Schedule: timeline over which RSUs become fully owned by the employee

Vesting Date: the date in which the GOOG shares are distributed into your account

Fair Market Value: value of the stock at any point in time

GSUs vest over a four-year period, with 25% vesting after the first year and the remaining 75% vesting in equal monthly installments over the following three years. However, the vesting schedule may differ, particularly for new hires or promotional grants. If you stay at the company for four years, you will receive all your GSUs. If you leave prior to that, you will lose those unvested shares.

Tax Implications and Your GSUs

There is no tax impact when you are granted new GSUs. The tax implications come when they vest, as well as when you sell the shares.

Once GSUs vest, they are taxed as ordinary income. Morgan Stanley will automatically withhold 22% of your vesting amount to cover your tax bill—like tax withholding from your paycheck. When you surpass $1M in supplemental income in a calendar year, withholding is readjusted to a 37% withholding rate. Withholding is covered by selling a portion of your shares. Many employees, especially those subject to the 22% withholding rate, often find that the automatically withheld amount is not enough to cover their full tax bill, so it is helpful to monitor your tax obligations.

If you hold onto your GSUs beyond the vesting date, your GSUs will be subject to capital gains taxation. The fair market value of the stock when they vest is the cost basis for these shares, and the sale price will determine your capital gain or loss, like with a typical stock sale. If you hold the shares for less than 1 year, those gains or losses will be treated as ordinary income. If you hold them for over 1 year, they will be taxed at capital gains rates.

The information shown below offers current tax rates for 2025.

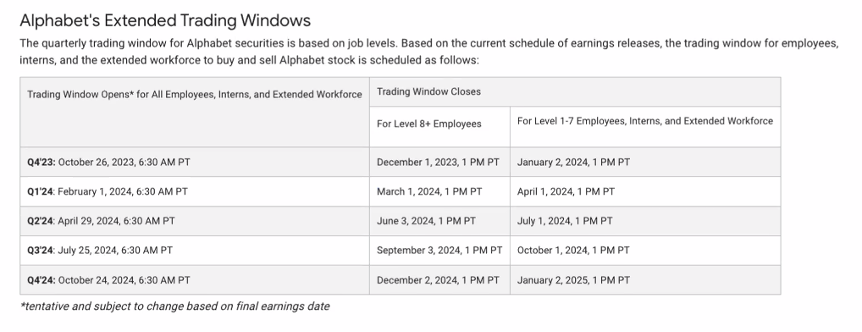

Google's Trading Windows and the Employee Trading Plan (ETP)

It's important to note that you cannot sell GSUs at any time. Instead, there are trading windows that will open for you, depending on your level and type of shares. This is designed to help prevent insider trading, similar to how a 10b5-1 plan works.

To get around this, Google offers an optional Employee Trading Plan (ETP) that allows employees to sell a predetermined amount of GSUs throughout the year, regardless of trading windows.

The main benefit of the ETP is that GSUs will automatically sell on their vesting date, taking the burden of deciding when to sell out of your hands. Additionally, the other benefits of enrolling in the ETP include:

Creates more predictable cash flow

Provides a more systematic approach to diversification through the enforced selling

Offers discipline and rational decision making rather than market timing

Some potential drawbacks of the ETP:

Lack of flexibility and control with selling GSUs – if you are enrolled in the ETP, you cannot sell any GOOG or GOOGL shares outside the plan or modify the automated trading schedule

Ultimately, enrolling in the ETP is something you need to consider in the context of your larger financial plan and your ability to abide by the plan’s parameters. If you do not enroll in the ETP, you can sell your Google stock during open trading windows (unless you have material, nonpublic information about Alphabet).

GSUs can provide excellent opportunities to build wealth for Google employees. As illustrated in this guide, there are many factors to consider, especially when it comes to tax implications and trading windows. Our team is well-versed in helping Google employees find the best path forward to meet goals that fulfill short and long-term financial needs.

Commas is a wholly-owned subsidiary of Truepoint Inc., a fee-only Registered Investment Adviser (RIA). Registration as an adviser does not connote a specific level of skill or training nor an endorsement by the SEC. More detail, including forms ADV Part 2A and Form CRS filed with the SEC, can be found at www.usecommas.com. Neither the information, nor any opinion expressed, is to be construed as personalized investment, tax or legal advice. The accuracy and completeness of information presented from third-party sources cannot be guaranteed.

Subscribe to newsletter

Subscribe to receive the latest blog posts to your inbox.

When it comes to giving back, there are a few tax-efficient strategies to make the most of your contributions and maximize your impact on the organization.

1️⃣ Qualified Charitable Distributions (QCDs): If you’re over 70½, the IRS allows tax-free IRA distributions directly to charity, reducing your tax burden and required minimum distributions!

2️⃣ Gifting Appreciated Stock: Instead of selling highly appreciated stock and paying capital gains, donate it directly! The charity pays no taxes, and you avoid capital gains, amplifying your impact.

Additionally, if you’re an Ohio resident, learn about the dollar-for-dollar Ohio SGO tax credit to directly support educational institutions here.

“When it comes to charitable giving, sometimes it can be something that kind of gets put on the wayside in terms of different things you can do in order to maximize your charitable giving. We have lots of clients that are charitably inclined and what we’re able to do is just maximize that gift by employing different strategies.

One of the strategies is called qualified charitable distributions. If you’re over 70 and 1/2, the IRS actually allows you to make tax-free distributions from your IRA to charitable organizations. And what this does is when you’ve been saving into your IRA, you’ve always been deferring those taxes so when you make this charitable distribution, you actually never pay taxes on it yourself and the charity never pays taxes on it. It’s a way that you could marginally increase the way that you’re giving. Another benefit to using qualified charitable distributions is that it this can ultimately lower your RMS your required minimum distribution. The more you get out of that IRA tax free and the more money giving from your IRA is lowering the required minimum distributions and ultimately lowering the amount of taxes you’ll pay on those dollars.

Another way to give charitably while maximizing tax efficiencies, is giving appreciated stock. A lot of organizations these days are able to take charitable donations in cash, but also in appreciated securities. What can happen is you’ve been gifted, maybe some really appreciated stock some legacy stock from grandparents or parents or maybe you bought stock years and years ago and you’ve never sold it and it’s been growing all these years. Now there’s a lot of built up capital gains in that fund, where if you were to sell it you, pay capital gains tax versus if you gift that share to charity, they receive it and do not pay taxes on it and you also have never paid taxes on that appreciation.”

Commas is a wholly-owned subsidiary of Truepoint Inc., a fee-only Registered Investment Adviser (RIA). Registration as an adviser does not connote a specific level of skill or training nor an endorsement by the SEC. More detail, including forms ADV Part 2A and Form CRS filed with the SEC, can be found at www.usecommas.com. Neither the information, nor any opinion expressed, is to be construed as personalized investment, tax or legal advice. The accuracy and completeness of information presented from third-party sources cannot be guaranteed.

Subscribe to newsletter

Subscribe to receive the latest blog posts to your inbox.

Investing in a Roth IRA is a great option for when you are younger in your career. By paying taxes upfront while you’re likely in a lower tax bracket, you’re setting yourself up for tax-free growth on that money for life. This means that when it’s time to enjoy your hard-earned savings later, both your contributions and gains can be withdrawn without any extra tax.

“The Roth IRA is one of our favorite accounts and the reason is: you make contributions into the Roth IRA and you say I’m okay paying the tax on these funds today, but we’re in historically low tax brackets. And when you’re younger in your career, hopefully you’re earning less than you will later in your career so the idea is that your tax bracket and the income that you’re making is only going to increase over time. So, while you’re in a lower tax bracket can we pay the tax today to get the money into the Roth where it can grow tax free for the rest of your life. So when you go to pull funds out of the Roth IRA, not only is that contribution that you made tax free, but so is all that growth.”

Commas is a wholly-owned subsidiary of Truepoint Inc., a fee-only Registered Investment Adviser (RIA). Registration as an adviser does not connote a specific level of skill or training nor an endorsement by the SEC. More detail, including forms ADV Part 2A and Form CRS filed with the SEC, can be found at www.usecommas.com. Neither the information, nor any opinion expressed, is to be construed as personalized investment, tax or legal advice. The accuracy and completeness of information presented from third-party sources cannot be guaranteed.

Subscribe to newsletter

Subscribe to receive the latest blog posts to your inbox.

As you prepare to say “goodbye” to 2024 and “hello” to 2025, here are a few smart financial planning moves to consider:

1. Make 2024 Contributions to IRAs (Individual Retirement Accounts) When? Before you file your taxes.

If it’s part of your financial plan, consider “maxing out” your IRA by 12/31. This means contributing the maximum allowable contribution: $7,000 if under age 50, and $8,000 if age 50 or above. If you don’t have the cash flow to contribute by 12/31, don’t worry! Just make sure you do so before you file your taxes next year.

2. Make 2024 Contributions to HSAs (Health Savings Accounts) When? Before 12/31.

If it’s part of your financial plan, consider “maxing out” your HSA by 12/31. This means contributing the maximum allowable contribution: $4,150 for individual coverage or $8,300 for family coverage. Be sure to include any HSA contributions made by your employer when calculating your eligible contribution amount. If you are not contributing to your HSA via payroll deductions, you have until you file your taxes to make the contribution.

3. Make 2024 Contributions to 529 Education Accounts When? Before 12/31.

For clients living in and contributing to 529s in states with a state income tax deduction for contributions (like Ohio), be sure to contribute to those plans before 12/31 to claim this year’s deduction.

4. Perform Conversions from Traditional IRA to Roth IRA When? Before 12/31.

For those that are planning to do the Backdoor Roth strategy, make the conversion from Traditional to Roth IRA by 12/31 in order to incur any applicable tax in the current year. As a Commas client, your advisor will perform the Backdoor Roth Conversion for you on accounts that we manage!

5. Take your Required Minimum Distributions from Retirement Accounts When? Before 12/31.

If you own a Traditional IRA or 401(k) and you have reached the age of 73, you must take your Required Minimum Distribution by 12/31. If you forget to take the distribution by the deadline, you may be subject to a 25% penalty on the shortfall.

As a Commas client, your advisor will make sure that you’ve taken distributions from the necessary accounts that we manage!

6. Own a Small Business? File the Beneficial Ownership Information Report (BOIR) When? Before 12/31.

Effective January 1, 2024, all existing and newly created small business entities will be required to file a beneficial ownership report to the Financial Crimes Enforcement Network (FinCEN) as part of the new Corporate Transparency Act. Please visit https://www.fincen.gov/boi for more information, including information regarding whether your small business entity is required to file, how to file, and a link to the BOIR online filing system. If you have any further questions, please reach out to your advisor.

7. Donate to Charity When? Before 12/31.

Donating to charity is an incredible way to support your community. It could also be a smart way to avoid capital gains taxes. Additionally, if you itemize your taxes instead of taking the standard deduction, charitable donations could enable you to deduct even more!

8. Check Your Beneficiaries When? Once annually.

It’s a good practice to check your beneficiaries on your accounts at least annually. A beneficiary will receive the funds in your account if you pass away. To check your beneficiaries on accounts, log onto your account’s custodian online to verify.

9. Line Up a Tax Specialist for Filing your Taxes When? By January.

Consider working with a tax professional, such as a CPA or EA, for your tax preparation. Not only will working with a tax professional make sure your taxes are filed accurately and on time, but it will save you time and reduce stress. If you’re interested in working with a tax professional and want a referral, please reach out to your advisor.

Commas is a wholly-owned subsidiary of Truepoint Inc., a fee-only Registered Investment Adviser (RIA). Registration as an adviser does not connote a specific level of skill or training nor an endorsement by the SEC. More detail, including forms ADV Part 2A and Form CRS filed with the SEC, can be found at www.usecommas.com. Neither the information, nor any opinion expressed, is to be construed as personalized investment, tax or legal advice. The accuracy and completeness of information presented from third-party sources cannot be guaranteed.

Subscribe to newsletter

Subscribe to receive the latest blog posts to your inbox.

Navigating Google’s 401(k) plan can be daunting, especially with the diverse options and features available. In this blog post, we will explain the components of the Google 401(k) plan. Our guide offers clear, useful tips for any Google employee looking to improve their current plans.

Three key aspects of Google’s plan that make it stand out from others in the industry.

Employer match program. Google will match 50% of your 401(k) contributions up to the pre-tax/Roth contribution limit. As of 2025, an employee can contribute up to $23,500 in pre-tax/Roth dollars. That means Google can add up to $11,750 in matching contributions to your account, if you contribute the maximum.

Even more notably, Google’s matching contributions vest immediately. In other words, you own 100% of the company’s contribution right away. This is true even if you leave the firm the day after the funds are deposited into your account.

Wide selection of investment funds. As a Google employee, you can choose from a diverse set of funds, including over 30 investment options —from target-date to individual index to actively managed funds. This broad selection enables employees to choose the right mix of investment vehicles to meet their unique set of priorities and goals.

Emphasis on flexibility. Google’s plan lets participants create their own tax strategy. They can contribute from pre-tax (Traditional), Roth, after-tax, bonus pre-tax, bonus Roth, and bonus after-tax dollars.

Three steps you can take today to maximize the Google 401(k) plan

As you consider how to tailor Google’s plan to meet your specific goals, here are three key actions you can implement.

Maximize your pre-tax/Roth contribution limit of $23,500. Given the impressive employer match, focus on maximizing Google’s contribution to your 401(k) plan. The more you contribute, the more Google will contribute, and they will do so until you hit the $23,500 limit. That’s an extra $11,750 of Google’s money, and it vests to your retirement account immediately.

If you can contribute $23,500 from your salary to your 401(k), consider adjusting your deferrals today. Otherwise, you are leaving free money on the table.

Take advantage of catch-up contributions. If you are 50 or older by the end of the year, you can contribute an extra $7,500 to your 401(k) in 2025. You can choose to make this contribution pre-tax or as a Roth contribution. Although these additional funds, commonly referred to as “catch-up contributions,” will not qualify for the employer match, they will help you save significantly more towards retirement.

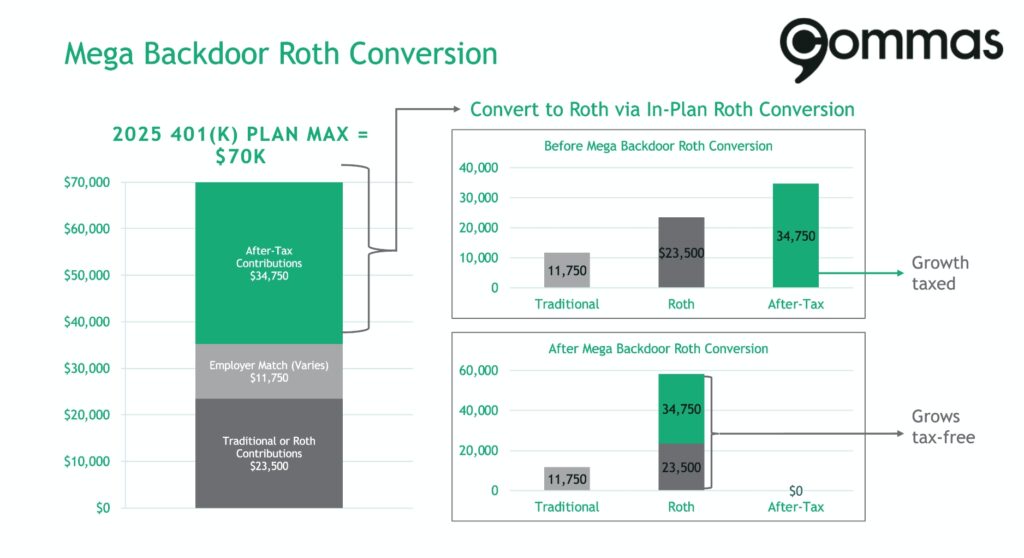

Consider after-tax contributions, especially for the mega backdoor Roth strategy. We want to be sensitive around balancing shorter-term goals with the goal of retirement, but if your budget allows, you can contribute even more to your plan than the $23,500 limit mentioned earlier. This limit applies to pre-tax and Roth contributions only. You can also make after-tax contributions to your 401(k). As of 2025, your 401(k) account can receive as much as $70,000 in contributions each year. This includes all the money deposited into the account—both from you and your employer.

For example, an employee contributes the maximum amount of pre-tax/Roth dollars ($23,500). Google matches 50% of that, which equals $11,750. In total, those contributions add up to $35,250—far short of the $70,000 limit. Therefore, this employee could still contribute another $34,750 in after-tax contributions to their 401(k) account.

Google also allows for in-plan Roth conversions, which completes the mega backdoor Roth strategy. You can learn more about the mega backdoor Roth strategy here.

Analysis paralysis: the biggest threat to your retirement plan

A highly flexible retirement plan like Google’s can provide enormous benefits but can also feel overwhelming. Probably the most common way people learn valuable “hacks” about their employer’s plan is through their coworkers. But those coworkers aren’t privy to the whole picture.

Consider the range of personal and professional questions you might be facing:

How do you balance saving for shorter-term goals (wedding, kids, house, etc.) with making sure you are on track for retirement?

How should your 401(k) be invested?

Should you be making pre-tax or Roth contributions?

Does maxing out after-tax contributions make more sense through your paychecks or using your annual bonus? How does this impact cash flow?

Should you prioritize debt or your 401(k)?

What should you do with your old 401(k) plans?

Your answers to these questions should directly inform your planning decisions. And they should make you cautious about simply opting for the plan’s default options—or taking the same approach as your colleagues.

Commas is a wholly-owned subsidiary of Truepoint Inc., a fee-only Registered Investment Adviser (RIA). Registration as an adviser does not connote a specific level of skill or training nor an endorsement by the SEC. More detail, including forms ADV Part 2A and Form CRS filed with the SEC, can be found at www.usecommas.com. Neither the information, nor any opinion expressed, is to be construed as personalized investment, tax or legal advice. The accuracy and completeness of information presented from third-party sources cannot be guaranteed.

Subscribe to newsletter

Subscribe to receive the latest blog posts to your inbox.

Landing a job at Google is a tremendous accomplishment. The company is not only a dynamic industry leader, staffed by innovative, top-of-the-line professionals. It also offers incredible salaries and a world-class benefits package.

At Google, your total compensation is the sum of your base salary, bonuses, and RSU grants (dubbed GSUs by Google employees). Beyond that, Google offers some incredible benefits related to the Google 401(k), Health Savings Account (HSA) match, life insurance, and long-term disability.

Health Savings Account (HSA) Match = $1k for individual plans and $2k for family plans

Tip: you must be in a high deductible health plan (HDHP) to be able to participate in a Health Savings Plan (HSA). Due to the amazing tax advantages of the HSA account, we love to recommend this to clients, but that doesn’t mean it is right for everyone. Taking into consideration your providers, health needs, if you will be having a baby that year, etc. is very important. Here are some tips on choosing a health plan.

Tip: The $1k and $2k employer contribution that Google offers counts towards the annual contribution limit of $4,150 for an individual and $8,300 for a family (+ $1k catch up if over 55).

Life Insurance = 3x salary up to $789,000

Tip: Be sure to add beneficiaries to your Google life insurance policy so that it passes to the appropriate people if something happens to you.

Tip: At Commas we will weigh if you need additional coverage – whether that is through voluntary coverage at Google or via the open market

Long-term Disability = 65% salary

Tip: There is no income cap on this, so the benefit will grow as your salary does. This is a benefit that you pay for however, that means that the benefit is tax-free to you if you need to claim disability.

You can find more details about your specific benefits in Moma. When you are hired—and each year during open enrollment—you will make your benefit selections via gBenefits. Here at Commas, we are happy to help you make those choices and review them annually.

Maximizing Your Awards

Think of the mix of salary, RSUs, and benefits that comprise your compensation as distinctive sources of wealth. Each has unique properties—advantages, as well as limitations—that enable you to achieve particular goals.

Commas is a wholly-owned subsidiary of Truepoint Inc., a fee-only Registered Investment Adviser (RIA). Registration as an adviser does not connote a specific level of skill or training nor an endorsement by the SEC. More detail, including forms ADV Part 2A and Form CRS filed with the SEC, can be found at www.usecommas.com. Neither the information, nor any opinion expressed, is to be construed as personalized investment, tax or legal advice. The accuracy and completeness of information presented from third-party sources cannot be guaranteed.

Subscribe to newsletter

Subscribe to receive the latest blog posts to your inbox.

Choosing the right health plan is based on your family’s needs and can make a big difference for your family’s healthcare costs.

An HDHP (High Deductible Health Plan) is ideal for healthy families who don’t often visit the doctor, offering lower premiums and the option to save tax-free with an HSA.

A PPO (Preferred Provider Organization) is great for families with more frequent medical needs, providing predictable costs per visit but higher premiums.

Not sure which plan fits your family? Your Commas advisor can help guide you through the decision during open enrollment.

“A high deductible health care plan or HDHP plan is one where you pay for all of your medical visits and procedures out of pocket in, generally, exchange for a lower premium each month or paycheck. The reason why these plans are called high deductible is exactly that. You have the opportunity to pay more out of pocket if you do frequent the doctor than say another health care plan. But that exchange is having a lower monthly premium. A PPO plan or a preferred provider organization health care plan is one where you pay specified costs for each visit or procedure and you know that ahead of time. However the trade-off, unlike the high deductible plan, is those premiums can tend to be more.

High deductible health care plans are great for families who are generally healthy, maybe don’t frequent the doctor as much. Which is great for those families because you’re not going to the doctor so you’re not paying out of pocket costs and also so you’re having lower monthly premiums. So all in all, if you’re healthy, that means more money in your pocket each month through each paycheck. With a high deductible plan you also have the option to use what’s called a health care savings account or an HSA account and how those work is you put money in pre-tax and if you’re using those to pay medical expenses they’re also tax-free. So essentially you never pay taxes on the money that you’re using to pay medical expenses.

A PPO plan is great for families who maybe need to visit the doctor or have more procedures done throughout the years because those costs of what that will be are known before even walking into those appointments so it can help families who may frequent the doctor more to plan financially how to pay for those costs. When it comes time for open enrollment your Commas advisor is here to help you decide which plan might be best for you and your family.”

Commas is a wholly-owned subsidiary of Truepoint Inc., a fee-only Registered Investment Adviser (RIA). Registration as an adviser does not connote a specific level of skill or training nor an endorsement by the SEC. More detail, including forms ADV Part 2A and Form CRS filed with the SEC, can be found at www.usecommas.com. Neither the information, nor any opinion expressed, is to be construed as personalized investment, tax or legal advice. The accuracy and completeness of information presented from third-party sources cannot be guaranteed.

Subscribe to newsletter

Subscribe to receive the latest blog posts to your inbox.

The 2024 presidential election cycle is in full swing. If you’re wondering how the upcoming election may impact your financial plan, check out the latest video from Commas Sr. Financial Advisor Josh Bentz.

“One question that we’re getting a lot right now from clients is: should I be worried about what’s happening with this upcoming election? Which is a valid concern, obviously there’s some tense things going on in the world. But our answer is: no, there’s really no correlation between your investment plan long term and the outcome of this election. The main trend that that we focus on for long-term investors is that the market provides the best source of returns for your long-term goals. And that is not really impacted by republicans or democrats or anything like that. That’s just how markets work. So if you’re a long-term investor, don’t worry about what happens in the next three to six months. Focus more on the long term. If you’re a short-term investor, you probably need to make sure you’ve got a plan in place that’s not going to be impacted by short-term moves in the market anyway.”

Commas is a wholly-owned subsidiary of Truepoint Inc., a fee-only Registered Investment Adviser (RIA). Registration as an adviser does not connote a specific level of skill or training nor an endorsement by the SEC. More detail, including forms ADV Part 2A and Form CRS filed with the SEC, can be found at www.usecommas.com. Neither the information, nor any opinion expressed, is to be construed as personalized investment, tax or legal advice. The accuracy and completeness of information presented from third-party sources cannot be guaranteed.

Subscribe to newsletter

Subscribe to receive the latest blog posts to your inbox.